Posted on Friday, August 2nd, 2019 in by Matt Garmony

July & August is when the Local Councils and Shires send out their annual Rates Notices. Landowners often question the amount of Council Rates that are required to be paid. In most circumstances, commercial property landowners pass the cost onto the tenants, who then dispute the amount of rates to be paid. Only the Gross Rental Value or GRV can be objected to. Not the rate in the dollar.

Council Rates are based on a rate in the dollar of the Gross Rental Value (GRV) assessed by the Valuer Generals Office at Landgate. Under the Valuation of Land Act 1978, “Any person liable to pay any rate or tax assessed in respect of land who is dissatisfied with a valuation of such land made under this Act, may serve upon the Valuer-General a written objection to the valuation.”

The Licensed Valuers at Garmony Property Consultants undertake numerous Valuations for the objection of the assessed Gross Rental Value and submit the prescribed objection form as their clients “Agent” and liaise with the Valuer Generals Office throughout the objection process.

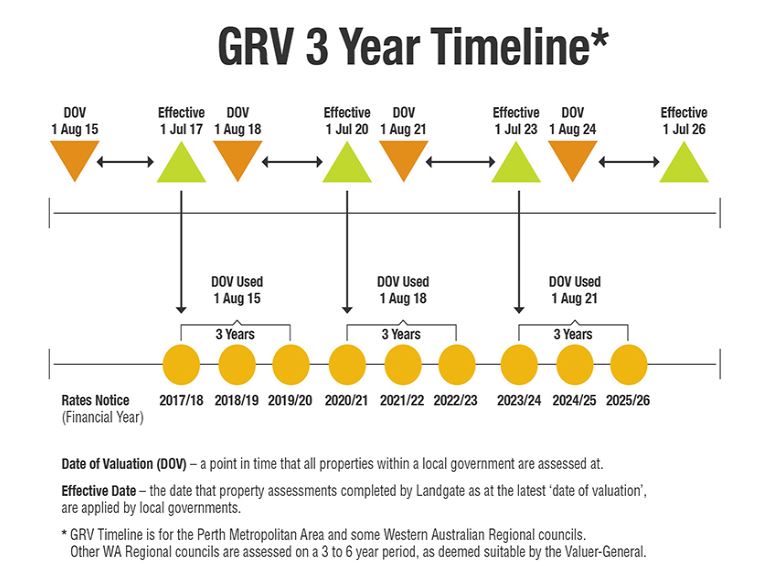

DATE OF ASSESSMENT

Gross Rental Values in Western Australia are assessed every 3 years on the 1st August (Assessment Date) and is then effective from the 1 July, two years after the Date of Valuation. The Effective Date is the date Local Councils will apply the GRV for the purpose of calculating your rates respectively. So, if you receive your Council Rate Notice for the 12 months commencing 1 July 2019, the Assessment date for the Unimproved Value will be 1 August 2015 as per the Landgate Timeline below;

If you feel the Gross Rental Value assessed by the Valuer General is above market levels as at the Date of Assessment or you are unsure what to do, please contact the expert Licensed Valuers at Garmony Property Consultants for further information. We can assist you with all your property related inquiries including Gross Rental Value objections for your Council Rates assessments. Click here to contact us. or www.garmony.com.au

DEFINITIONS

The Valuation of Land Act defines Gross Rental Value or GRV as;

gross rental value of land means “the gross annual rental that the land might reasonably be expected to realize if let on a tenancy from year to year upon condition that the landlord were liable for all rates, taxes and other charges thereon and the insurance and other outgoings necessary to maintain the value of the land”

However in some situations if the GRV cannot reasonably be determined on such basis as defined by the Act above, then the gross rental value shall be the assessed value and if the value of the improvements of land not used for residential purposes is less than one-third of the vacant land value, then the GRV will be assessed value.

Assessed value of land means such percentage of the capital value of the land as may from time to time be prescribed either —

(a) in respect of land generally; or

(b) in respect of a class of lands which includes the land;

capital value of land means the capital amount which an estate of fee simple in the land might reasonably be expected to realize upon sale — provided that where the capital value of land cannot reasonably be determined on such basis, the capital value of such land shall be the sum of, first, the unimproved value of the land, and, secondly, the estimated replacement cost of improvements to the land after making such allowance for obsolescence, physical depreciation, and such other factors as are appropriate in the circumstances;

The percentages used above is 3% for Residential and 5% for non-residential land under the Valuation of Land Regulations 1979.

This means for underutilised sites such as old houses converted to office use in redevelopment areas, where the improvements add little value (generally a holding income until redevelopment) then the Gross Rent may be less than 5% of the Land Value and the higher of the two assessments will be used as the GRV for rating and taxing purposes.

CASE STUDY – Converted House on small development site in South Perth.

The property has a tenant paying a Net Rent of $50,000 per annum (inclusive of GST) plus outgoings of $15,000 which indicates a Market Gross Rent of $65,000. However the Assessed Land Value (Unimproved Value or UV) of the property is $1,800,000. If the improvements add less than $600,000 (in this case they only add $150,000) then the site is considered underdeveloped and therefore the 1/3 rule applies. The Assessed GRV (or Site Value GRV) would be 5% of the land value of $1,800,000 being $90,000 and not $65,000 as what is paid by the market.

The above case study shows that the GRV assessment by the Valuer General may appear to be above market levels or unfair, however the definition of Gross Rental Value in the Valuation of Land Act 1978, the assessment complies.

Please contact the expert Licensed Valuers at Garmony Property Consultants for further information and advice on Gross Rental Valuation and Unimproved Value objections for your Council Rates and Land Tax assessments.

UNIMPROVED VALUE FOR LAND TAX

The annual Unimproved Value Assessment for Land Tax is different to the Gross Rental Valuation (GRV) used for Council Rates and Taxes. In Western Australia the Unimproved Value (UV) is assessed at the same date each year being the 1 August (Assessment Date). This date is used by valuers to ensure a fair and equitable assessment is completed for all land. The Unimproved Value is then effective from the 1 July the following year which is when the Office of State Revenue and some local councils will apply the UV for the purpose of calculating your taxes or rates respectively. So, if you receive your Land Tax Notice for the 12 months commencing 1 July 2019, the Assessment date for the Unimproved Value will be 1 August 2018;

Our previous UV Blog provides further details in this regard. (Click here)