Unimproved Value Objections for Land Tax Assessments

The Department of Finance – Office of State Revenue’s Land Tax notices are being delivered to landowners. The Government has not altered rate in the dollar amount for the calculation of Land Tax payments based on the assessed Unimproved Land Value. Landowners often question the amount of Rates that are required to be paid. In most circumstances, commercial property landowners pass the cost of Land Tax onto tenants, who then dispute the amount of rates to be paid. Only the Unimproved Value or UV can be objected to. Not the rate in the dollar. This requires an Unimproved Value Objections for Land Tax Assessments purposes.

Land Tax is an annual tax, based on a rate in the dollar of the Unimproved Value (UV) of the land, assessed by the Valuer Generals Office at Landgate. Under the Valuation of Land Act 1978, “Any person liable to pay any rate or tax assessed in respect of land who is dissatisfied with a valuation of such land made under this Act, may serve upon the Valuer-General a written objection to the valuation.”

The Licensed Valuers at Garmony Property Consultants undertake numerous Valuations for the objection of the assessed Unimproved Value. We can submit the prescribed objection form as your “Agent” and liaise with the Valuer Generals Office throughout the objection process.

The Valuation of Land Act 1978 defines Unimproved Value or UV as;

unimproved value means —

(a) in relation to any land situate within a townsite, except land referred to in paragraph (b)(ii), the site value;

site value of land means the capital amount that an estate of fee simple in the land might reasonably be expected to realize upon sale assuming that any improvements to the land, other than merged improvements, had not been made and, in the case of land that is reserved for a public purpose, assuming that the land may continue to be used for any purpose for which it is being used or could be used at the date of valuation;

DATE OF ASSESSMENT

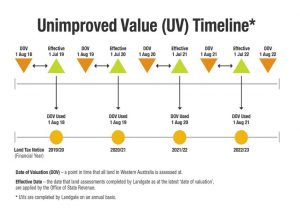

Source: Landgate

All land in Western Australia is assessed at the same date each year, being the 1st August (Assessment Date) to determine its Unimproved Value (UV). This date is used by valuers to ensure a fair and equitable assessment is completed for all land. The Unimproved Value is then effective from the 1 July the following year. This is the date which the Office of State Revenue and some local councils will apply the UV for the purpose of calculating your land taxes or rates respectively. So if you receive your Land Tax Notice for the 12 months commencing 1 July 2021, the Assessment date for the Unimproved Value will be 1 August 2020 as per the Landgate Timeline below;

This annual Unimproved Value (UV) Assessment is different to the Gross Rental Valuation (GRV) used for Council Rates and Taxes. The GRV is assessed every 3 years in the Metropolitan Area and every 3-6 years in regional areas. The date of valuation for the GRV assessment was 1 August 2015 and the effective date was 1 July 2017, 1 July 2018 & 1 July 2019. The next Assessment date for the GRV is 1 August 2018 and the effective dates will be 1 July 2020. Our previous GRV Blog provides further details in this regard. (Click here).

If you feel the Unimproved Value assessed by the Valuer General is above market levels as at the date of assessment, or you are unsure what to do, please contact the expert Licensed Valuers at Garmony Property Consultants for further information on Unimproved Value objections for Land Tax purposes. Please note you only have 60 days from the date of the Land Tax Notice to lodge an objection. We can assist you with all your property related inquiries including Unimproved Value objections for Land Tax purposes. Click here to contact us regarding Unimproved Value Objections for Land Tax Assessments purposes.